“Private credit doom” has been a recurring headline for a year. However, what is actually happening with private credit, and how is it connected to the SaaSpocalypse?

This article by Juan Ignacio Garcia works through what is really going on inside the asset class, why the 2020 to 2023 vintages have produced real but contained losses, and what the recalibration means for tech founders. Whether you are preparing for a sell-side process or raising structured debt for acquisitions, the cycle in private credit affects what you can do, when, and on what terms.

The rise of private credit: a $4 trillion asset class in 15 years

The 2007 to 2009 financial crisis had long-standing consequences in the financial industry that trickled to the overall real economy, notably through changes in global banking regulations.

Two asset classes were significantly affected: real estate and mortgage lending, and long-term corporate loans. The first one is perhaps what most immediately impacted people's lives, with larger equity requirements for individuals to buy homes and very limited options for developers to fund their projects, which, coupled with increased urban concentration, has left a global housing crisis with no end in sight. The second one is the focus of this article: banks have almost completely withdrawn from long-term corporate lending.

This has left an open space for private credit funds that have developed flexible, varied strategies. However, given that their whole business model relies on charging management fees, promising high returns to investors, and harvesting carried interest, they have tended to flock only into highly remunerated asset classes.

One particular type of loan that has proven attractive to private credit funds is financing buyout deals. With a simple and scalable origination and go-to-market strategy, by just targeting private equity funds instead of end borrowers, and a type of client whose incentives clearly align with their own, they quickly took over leveraged finance, eroding banks' market share even further when interest rates hiked.

Within 15 years, the asset class has grown to approximately $4 trillion in total assets, with around $3.2 trillion deployed once dry powder is excluded.

Software and technology companies account for roughly 20% of private credit exposure, doubling to around 40% if IT services are included. That puts close to $800 billion of credit deployed in software borrowers. The overweight has two causes: software companies lack the tangible assets banks traditionally used as collateral, and recurring subscription revenue has been treated as stable long-term cash flow.

What's under the rug: the 2020 to 2023 vintage problem

Something is already in the open and has been for a while: the 2020-23 vintages were ugly, and there are plenty of latent losses there. See the below chart and be aware that things have gotten notably worse since when it was published (data as of December 2024).

The very recent Medallia handover is only an example of what went wrong those days: buyouts of thin or no profit companies at more than 10x revenue, with deal leverage still being at 40 to 60%. The play during those years was hyper growth and the hope for a 3 to 4 year exit that would refinance all the debt. With the structures on offer (bullet maturities, PIK or elective cash interest, covenant-lite) these were quasi-equity bets dressed as debt. When growth slowed and multiples reset in 2022 and 2023, the math broke.

A structural complication sits underneath all of this. Most leveraged buyout debt is structured for limited debt service through its life: bullet maturities, covenant-lite terms, PIK or elective cash interest. The health of the loan depends on the health of the borrower, not on debt service metrics. Valuation methodologies are accordingly looser than they should be; guidelines from FASB, IASB, and SEC's rule 2a-5 give fund managers wide latitude to mark positions in their books. Take Medallia: creditors marked their position down 25%, implying recovery at 5x revenue. Whether that holds in the current market is a generous assumption.

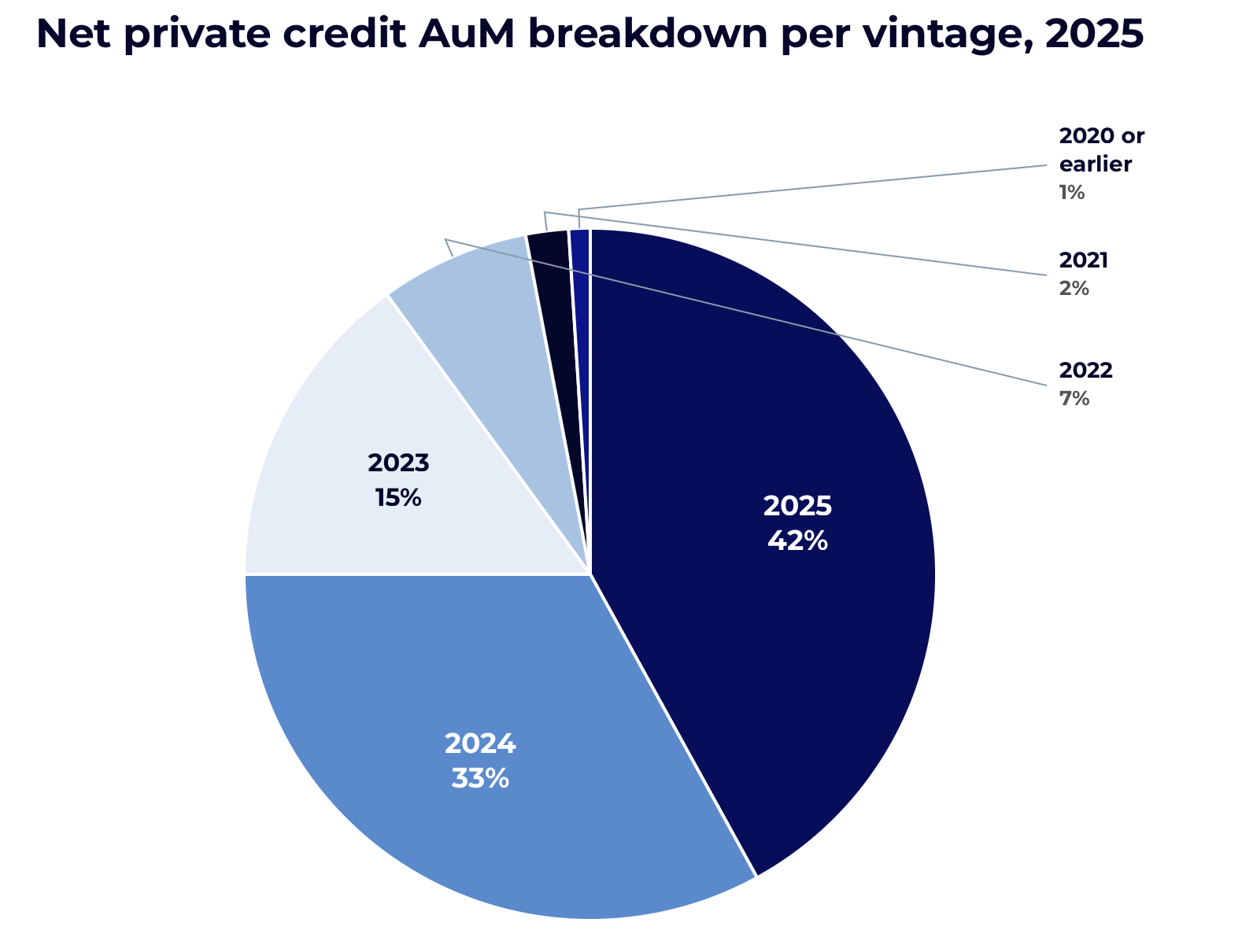

So how big is the hole? The 2021 vintage represents a small fraction of current net assets under management. Deployment has grown significantly since, and most of the loans deployed in those bad vintages have either rolled or been written down already.

Below is my estimate vintage breakdown of current AuM (ex dry powder) as of today, based on the most recent ACC survey on AuM and deployment per year, with estimated repayments based on a c. 5-year average maturity.

The picture going forward is healthier, though not clean. With multiples contracted, leverage on the 2025 tech cohort is closer to 3x revenue rather than the 5x or 6x of 2021. That should be low enough to service cash interest in most cases. But the EBITDA/Interest coverage ratio across private credit transactions averages 2x across all sectors, and tech sits below that average because tech borrowers tend to have thin EBITDA to begin with. Refinancing risk has not gone away. It has been pushed forward, into the cohort that will be looking to refinance in 2027 and 2028.

A broader question follows from this, and one worth flagging for future analysis: if private credit has skeletons in the closet, and private credit is leveraging private equity, how tidy is PE's closet? That is a different article.

SaaS private credit: why this isn't 2008

Private credit will have to purge a few years of exuberance. The question is whether this is doomsday for the asset class, or for the tech borrowers inside it. The answer, on both counts, is no.

There is no systemic risk in any of this, for three reasons. First, the 2020 to 2023 vintages represent a small fraction of current net assets under management. Deployment has grown materially since. Second, these are closed-end fund structures with no deposit holders. Investors are pension funds and institutional allocators absorbing a cyclical loss, not retail account holders triggering a run. Third, the dry powder waiting to be deployed is close to $1 trillion, and global liquidity remains at peak levels.

Reported private credit returns are still in low double digits, though recent asset-level data suggests several reputable managers will need to recognize losses that compress those numbers further. The result is a purge and reset, not a collapse. Funds will redeploy under modified policies, write the cycle off, and the top quartile of managers will take share from the bottom.

What it means for SaaS valuations in 2026

For mid-market SaaS founders, the practical impact is more nuanced than "valuations are down." Three things are shifting.

- Leverage policy is self-adjusting, not collapsing. Lower revenue multiples on new deals mean automatically lower absolute leverage, even if the percentage policy holds. A 6x revenue buyout at 50% leverage is a smaller dollar loan than an 8x revenue buyout at 50% leverage was in 2021. This alone does not compress your bid. Compression only happens if funds shift their LTV policy from 40 to 60% down to 25 to 40%. The base case is that they hold policy on quality assets and tighten on edge cases.

- Bifurcation between clean and AI-exposed SaaS sharpens. PE and private credit funds will continue partnering to buy out best-in-class software companies at strong multiples. They will steer clear of assets with AI-related existential risk or weak SaaS metrics. The middle of the market thins out faster than the top.

- Refinanceability stress tests get stricter. Because most LBO debt structures rely on a successful exit to repay (PIK, covenant-lite, bullet structures), buyers are stress-testing whether your business will be exit-ready in three to four years. AI exposure now sits at the top of that question list, alongside customer concentration, NRR durability, and the realism of forecast revenue growth.

What it means for your sell-side process and debt strategy

The buyer composition of your sell-side process arguably matters more in 2026 than it did in 2021. For clean, high-NRR, profitable SaaS, direct PE platform formations and PE-backed platform add-ons compete actively, with selective interest from strategic acquirers pursuing AI or cybersecurity theses. The capital is there and the underwriting math works for premium assets, therefore, run a tight, structured competitive process. This is where a disciplined approach produces the best outcomes.

For mid-tier or AI-exposed SaaS, the realistic buyer set narrows. Direct strategic acquirers are largely on hold for transformational mid-market deals. Direct PE platform formations are more selective. PE-backed platforms running add-on programs become the dominant active buyer. Hence, the process design changes accordingly: instead of a wide sweep, the work is identifying which platforms have active vertical mandates that fit your business and engaging them with a thesis-aligned narrative. Recent M&A trends in 2026 already point to this concentration and private credit dynamics reinforce it.

For founders raising structured debt to fund acquisitions or build a rollup platform, the same recalibration affects you directly. Funds tightening underwriting means stricter coverage tests, more conservative LTVs on new acquisitions, and less appetite for hyper-growth structures with negligible EBITDA. It also means top quartile managers continue to deploy aggressively for clean businesses and well-conceived platforms. The terms you can negotiate depend on which lenders are competing for your facility, what their cycle position is, and how clearly your business case maps to refinanceable cash flow. This is the lens L40° sees from both sides of the deal stack, advising founders on sell-side outcomes and on raising structured debt for acquisition financing and rollups.

So, in brief:

- Latent losses in private credit are real. The 2020 to 2023 vintages will produce write-downs that have not yet fully surfaced in reported returns.

- There is no systemic risk in those losses. Closed-end fund structures, no deposit holders, close to $1 trillion of dry powder, and global liquidity at peak levels.

- Funds will continue deploying under modified policies. A return to bank-led corporate lending is unlikely. Tighter regulation is more probable, particularly on reporting and valuation methodologies.

- Tech valuations will see selective compression. The impact will discriminate between good and bad assets. Premium multiples on clean SaaS metrics. Sharper underwriting on AI-exposed or thin-EBITDA assets.

For founders, this is a market that rewards preparation, clarity on metrics, and a credible narrative on AI defensibility. Whether you are running a sell-side process or raising structured debt for acquisitions, understanding which side of the bifurcation you sit on, and shaping your story accordingly, is what separates premium outcomes from the rest. Talk to L40° about your exit.

Recommended

- M&A Trends for 2026: What Tech Founders Should Expect

- The AI Wrappers Debate: How to Value Them?

- AI Rollups in 2025: What Founders Need to Know

- SaaS Multiples: Valuation Benchmarks for 2025

A longer technical version of this analysis was first published on Juan Ignacio García's Substack.